Tampa Impact Windows: How Much Can You Save on Homeowners Insurance?

May 20, 2026

On this page

If you own a home in Tampa, you already know what’s happening to your Florida homeowners insurance bill. Rates have surged dramatically over the past several years, leaving many families scrambling for ways to offset those costs. One of the most effective and financially rewarding solutions available to Tampa homeowners right now is investing in tampa impact windows. Not only do they offer superior hurricane protection, they can directly reduce what you pay for insurance every single year. How much could you actually save? Let’s break it down.

Florida’s insurance crisis isn’t a temporary blip. Insurers are pulling out of the market, and those that remain are charging more than ever to cover the mounting risk of hurricane damage. For homeowners in Tampa a city sitting squarely in one of the most storm-prone corridors in the country the financial exposure is very real. But there’s good news: impact resistant windows represent one of the most impactful home improvements you can make, both for safety and long-term financial savings.

Ready to see your potential savings? Contact us for a FREE estimate and wind mitigation consultation today.

Why Florida Insurance Rates Are Skyrocketing

Florida’s homeowners insurance market is in a state of crisis. Over the past decade, major insurers have either left the state entirely or raised premiums to levels that many families find difficult to sustain. Several factors are driving this trend:

- Hurricane frequency and intensity: The Gulf Coast, including the Tampa Bay region, faces an elevated risk of direct hurricane hits. Climate data consistently shows storm intensity increasing over the Gulf of Mexico, putting coastal and near-coastal properties at elevated risk.

- Insurance company insolvencies: Multiple Florida insurance carriers have become insolvent since 2020, forcing tens of thousands of homeowners into Citizens Property Insurance the state’s insurer of last resort.

- Reinsurance cost spikes: When private insurers pay more for their own backup coverage, those costs get passed directly to homeowners.

- Litigation and fraud: Florida accounts for a disproportionate share of homeowners insurance litigation nationwide, which adds overhead costs across the industry.

For Tampa homeowners specifically, the combination of hurricane exposure and a volatile insurance market creates a perfect storm of financial pressure. The good news is that you have leverage and that leverage comes in the form of documented, certified storm protection windows that insurers are required to reward.

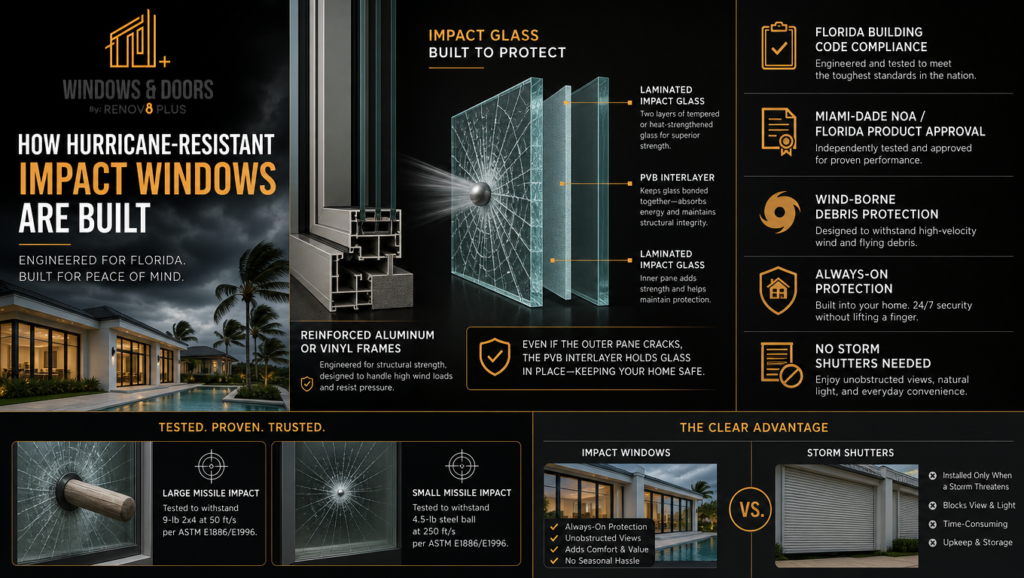

What Are Impact Windows?

How Impact Windows Lower Your Homeowners Insurance Costs

The link between storm protection windows and insurance discounts is straightforward: insurers charge premiums based on risk. When you reduce your home’s vulnerability to hurricane damage, you reduce the insurer’s expected payout and they reward that reduction. Here’s how the process works:

- Risk assessment: Your insurer evaluates the likelihood and severity of claims from your property. Homes without impact-rated openings are considered high-risk in wind zones like Tampa.

- Wind mitigation inspection: A licensed Florida inspector evaluates your home’s wind resistance features roof covering, roof deck attachment, roof-to-wall connections, and critically, opening protections like impact windows or shutters.

- Mitigation credits applied: The inspection report is submitted to your insurer, who then applies mandated discounts based on the level of protection present.

- Annual premium reduction: You receive a lower premium often permanently as long as your impact windows remain in place and meet code requirements.

The wind mitigation inspection is not optional it’s the mechanism through which your investment gets recognized by your insurer. Without it, you may be paying for protection but not receiving the financial credit you deserve.

Ask us about scheduling your wind mitigation inspection we assist Tampa homeowners throughout the process.

Citizens Property Insurance Discounts Explained

Citizens Property Insurance is Florida’s state-run insurer and one of the largest providers in the Tampa Bay area. Under Florida law, Citizens is required to offer insurance discounts for verified wind mitigation features including impact resistant windows.

Opening Protection Credits

Citizens uses the wind mitigation inspection report to assess your home’s “opening protection” level:

- No protection (basic): No credit applied. Standard premium.

- Shutter protection: Partial credit, since shutters require manual deployment and may not cover all openings.

- Impact window protection (all openings): Maximum opening protection credit applied often the largest single discount category available.

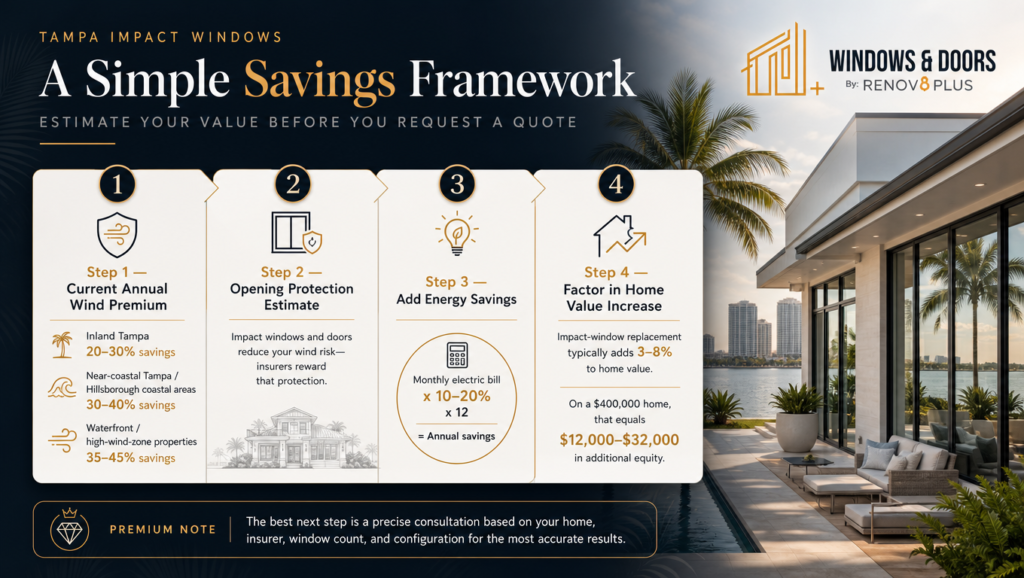

Discount Percentage Ranges

The opening protection credit from Citizens can range from approximately 15% to 45% of your wind premium, depending on:

- Your home’s construction type and age

- Roof type and condition

- Whether all openings including garage doors and skylights have impact protection

- Your location within the state’s wind speed zones

Protection Level | Typical Credit Range | Annual Savings (Est.) |

No protection | 0% | $0 |

Partial shutters | 10-25% | $250-$800 |

Full impact windows (all openings) | 25-45% | $600-$3,000+ |

Note: Credits apply to the wind portion of your premium. Total annual savings depend on your specific policy structure and home profile.

Shutters vs. Impact Windows: Which Gets More Credit?

Both shutters and hurricane windows can qualify for opening protection credits, but impact windows tampa fl typically earn higher credits for several reasons:

- Impact windows protect 24/7 no deployment required

- Shutters must be properly installed and rated to qualify many older shutter systems no longer meet current code

- Some insurers view always-on protection as significantly lower risk

- Impact windows satisfy multiple inspection categories simultaneously, compounding the discount

Typical Insurance Savings for Tampa Homeowners

Claim Reduction Data & Long-Term Financial Benefits

Impact resistant windows also dramatically reduce the likelihood that you’ll file a hurricane damage claim which has its own compounding financial benefits.

- Water intrusion prevention: The majority of hurricane-related home damage is from water intrusion through broken windows and doors. Impact windows eliminate this vulnerability.

- Fewer claims = lower premiums long-term: Filing claims raises your premiums and can trigger non-renewal. Homeowners with impact windows rarely file storm-related claims, protecting their insurance history.

- Deductible savings: Florida homeowners typically carry a separate hurricane deductible of 2-5% of their home’s insured value. On a $400,000 home, that’s $8,000-$20,000 out of pocket. Impact windows help you avoid reaching that threshold.

- Post-storm livability: Homes with impact windows are far more likely to remain habitable after a hurricane, saving hotel costs, storage fees, and the stress of temporary displacement.

Energy Savings: The Other Financial Benefit of Impact Windows

Not all impact window companies are created equal. Choosing the right installer is just as important as choosing the right product a poorly installed impact window may not perform as rated, and could jeopardize your insurance discount eligibility.

What to Look For in Impact Window Companies

- Florida Contractor License: Only hire window contractors licensed by the Florida Department of Business and Professional Regulation (DBPR). Verify their license status before signing any contract.

- Product approvals and certifications: The windows must carry a Florida Product Approval number or Miami-Dade County NOA. Ask to see the documentation.

- Installation permits: Legitimate impact window companies always pull permits. Permit-free installations are a major red flag that could void your warranties and prevent insurance credit qualification.

- Manufacturer warranty: Look for products backed by a lifetime or 20+ year warranty from the manufacturer, plus a workmanship warranty from the installer.

- Local Tampa experience: Companies with deep roots in the Tampa market understand local building codes, inspector preferences, and products that perform well in Tampa’s coastal environment.

- References and reviews: Ask for references from local homeowners who’ve gone through the wind mitigation inspection process. Verified Google reviews and BBB ratings matter.

When evaluating impact window companies, prioritize transparency about the installation process, timeline, and what to expect during the permit and inspection stages. A reputable company will walk you through every step including assisting with your wind mitigation inspection and insurance discount verification.

Is the Investment Worth It? A Clear ROI Analysis

Let’s do the math on a realistic Tampa homeowner scenario:

Example: 2,000 sq ft Tampa Home ROI Breakdown Impact window installation cost: $18,000 Annual insurance savings: $1,800 Annual energy savings: $500 Total annual financial benefit: $2,300 Estimated payback period: ~7.8 years Increased home value (est. 5-8%): $12,000-$18,000 |

Beyond the raw financial return, there are intangible benefits that are difficult to price: the peace of mind of knowing your family is protected during a hurricane, the elimination of the stressful annual shutter-hanging ritual, and the comfort of a quieter, more energy-efficient home.

Florida’s real estate market consistently rewards homes with certified hurricane protection. Buyers in Tampa actively seek out homes with impact resistant windows and they’re often willing to pay a premium for the reduced insurance costs and storm safety that come with them.

Estimate Your Potential Savings: Tampa Homeowner Guide

See How Much You Could Save — Request Your Free Estimate and Insurance Savings Analysis Today

Frequently Asked Questions About Tampa Impact Windows & Insurance

Q: How much do impact windows reduce homeowners insurance in Florida?

Impact windows can reduce your Florida homeowners insurance premium by 15% to 45%, depending on your insurer, home profile, and whether all openings have impact protection. The exact savings are confirmed through a certified wind mitigation inspection.

Q: Do I need a wind mitigation inspection after installing impact windows?

Yes. A wind mitigation inspection by a licensed Florida inspector is required to receive insurance discounts. The inspection verifies that your impact resistant windows meet current Florida Building Code standards and documents their specifications for your insurer.

Q: Do impact windows qualify for Citizens Property Insurance discounts?

Yes. Citizens Property Insurance is required by Florida law to offer opening protection credits for verified hurricane resistant windows florida-compliant products. Your discount amount depends on your inspection results and home characteristics.

Q: How long does it take to recoup the cost of impact windows?

Most Tampa homeowners see a payback period of 7 to 12 years when combining annual insurance savings with energy savings and increased home value. Homes with higher premiums particularly coastal and waterfront properties often see faster returns.

Q: Are impact windows worth it compared to storm shutters?

For most Tampa homeowners, yes. While shutters have a lower upfront cost, hurricane windows provide 24/7 protection, require no manual deployment, offer energy savings, provide noise reduction, and typically earn higher insurance discounts. Over a 10+ year horizon, impact windows often have a superior total financial return.

Q: Can impact windows increase my home’s resale value?

Impact glass windows are a highly sought-after feature in Florida’s real estate market. They signal lower insurance costs, storm safety, and energy efficiency to prospective buyers all factors that support a higher sale price.

Q: What certifications should I look for when choosing impact window companies?

Look for impact window companies whose products carry Florida Product Approval numbers or Miami-Dade County NOA designations. The installing contractor should hold a current DBPR license, and all work should be permitted and inspected by your local building department.